- TAX LAWYERS, TAX ADVISORY, TAX COMPLIANCE, EXPATS - SYDNEY, BRISBANE, MELBOURNE, CANBERRA

- 1300 334 518

- admin@waterhouselawyers.com.au

Accessing your Australian Superannuation

Superannuation

Accessing your Australian Superannuation

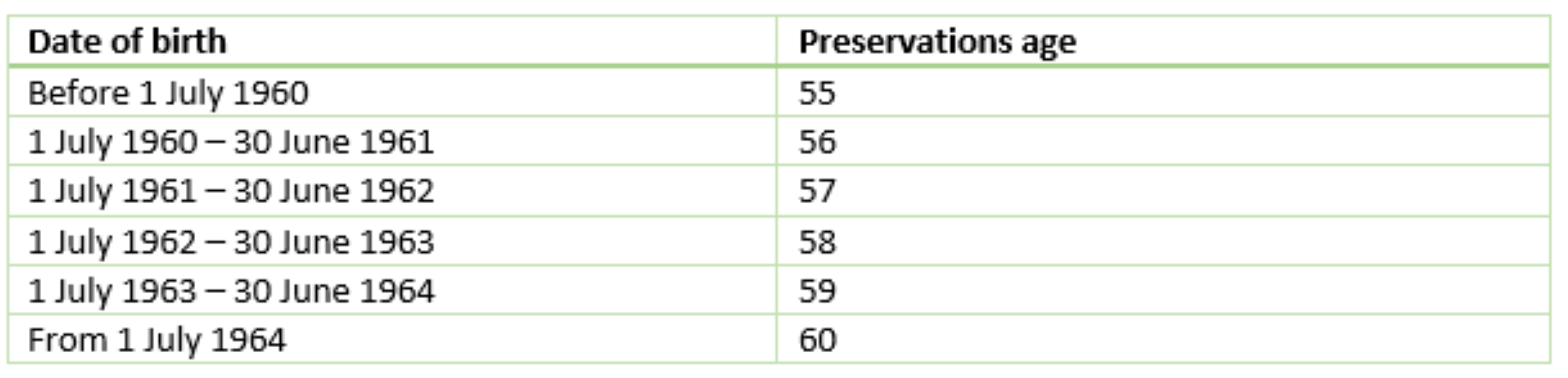

Accessing superannuation funds can be tricky prior to reaching your preservation age. Those born before 1 July 1964, can access their superannuation funds prior to age 60. Those born on or after 1 July 1964, have to meet a condition of release or reach age 60 to access their funds.

Accessing superannuation at preservation age

Between age 55 and 65, there are multiple ways your superannuation can be accessed, with various tax consequences as discussed below.

In general, you are able to access your superannuation once you have met your preservation age or once you have met a condition of release. The tax consequences differ depending on when you begin to access your super.

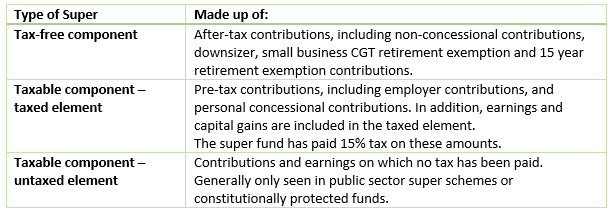

Superannuation components

Superannuation is made up of three components: tax-free, taxable component-taxed element, and taxable component – untaxed element. Each component is made up of different types of contributions and earnings. The different components are differentiated for tax purposes.

Accumulation versus Retirement phase

The accumulation phase of superannuation is the time period in which the member is actively making contributions and is growing the superannuation fund wealth. The retirement phase of superannuation begins when you move from the accumulation phase and commence a pension.

A fund can be in both phases at the same time, as discussed below. The tax treatment of earnings and capital gains is determined by which phase the fund is in.

Between 55 and preservation age

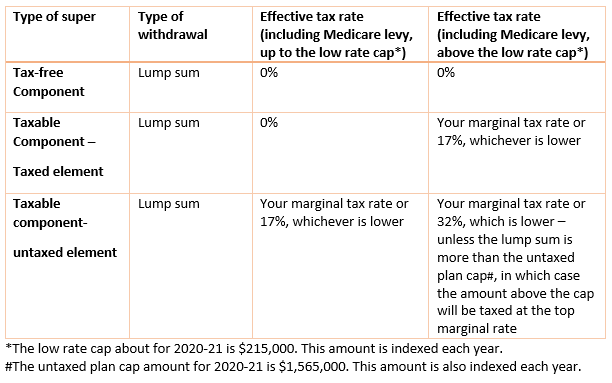

A member is only able to access superannuation prior to preservation age, if they have met a condition of release, or specific requirements for certain defined benefit funds such as CSS.If you are able to access your lump sum benefit between age 55 and preservation, the tax treatment would be as follows:

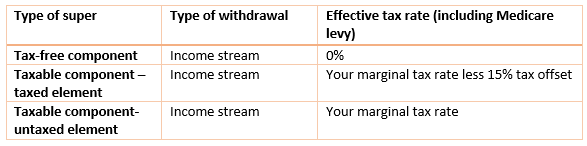

The tax rate of income stream before meeting preservation age are as follows:

Money in the fund in accumulation will continue to have earnings and capital gain taxed at 15% and 10% respectively.

Between preservation age and before 60

Accessing accumulation

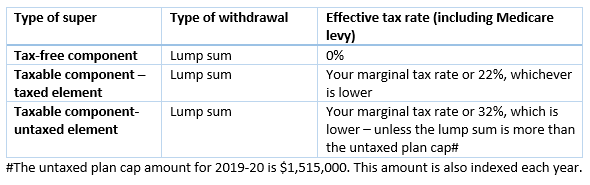

If you have not commenced an income stream, as discussed above, the only withdrawal option is a lump sum. The taxation of lump sums is complex and subject to different caps. The ATO website has a summarised table of all the different tax outcomes when interacting with different caps.

If you are able to access your lump sum benefit, the tax treatment would be as follows:

Accessing an income stream

A Transition to Retirement Income Stream (‘TRIS’), allows people who have reached their preservation age to have access to their superannuation benefits without having to retire or leave their job. A TRIS may be suited to those who have not yet met a condition of release.

Key aspects of a TRIS are:

- Minimum age-based pension withdrawals

- Maximum 10% withdrawal limit per year

- Unable to take lump sums

- Not a retirement phase income stream

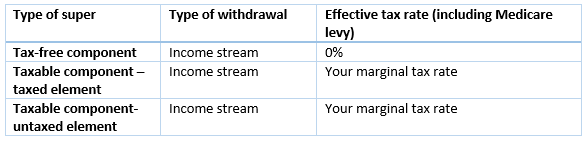

The tax rate of income streams taken between preservation age and 60 are as follows:

A TRIS is not a ‘retirement’ phase income stream. The superannuation fund will still be in the accumulation phase, and any earnings will be taxed at 15% and capital gains at 10%. In addition, the members Transfer Balance Cap will not be triggered.

Once the member meets a condition of release, the TRIS can be converted to a retirement phase income stream, such as an Account-Based Pension (‘ABP’). At this point, a Transfer Balance Cap event will be triggered.

If the member has met a condition of release and preservation age, the member will be able to access an Account-Based Pension (‘ABP’). The ABP provides more flexibility, however until you reach 60, the taxable component of withdrawals will continue to be taxable to the individual.

Key aspects of a TRIS are:

- Minimum age-based pension withdrawals

- No maximum withdrawal

- Can take lump sums (however will not count towards minimum pension)

- Retirement phase income stream

As ABP are in retirement phase, any earnings or capital gain relating to the income stream will be tax free within the fund.

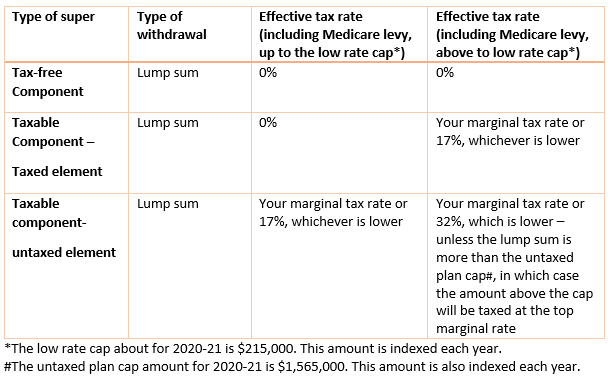

Lump sum taken from an ABP are taxed as follows:

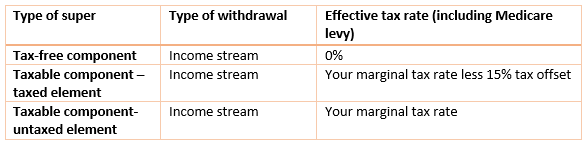

Pension withdrawals taken from an ABP are taxed as follow:

With both an ABP and TRIS, no capital (contributions) can be added to the income stream. Earnings and capital gains can increase the income stream balance, while withdrawals will result in draw down of your superannuation funds.

Accessing Superannuation 60 and over

If you have not met a condition of release by age 60, you will only be able to commence a TRIS. The tax-free and taxed component of any pensions you take from a TRIS will be tax-free. However, earnings and capital gains will continue to be taxed in the fund, until the TRIS is converted to a retirement phase income stream.

If you have commenced an ABP, the pension withdrawals will be tax free (subject to any untaxed component). Earnings and capital gains will continued to be tax-free within the fund as well.

If you receive a defined benefit income stream, such as MilitarySuper/CSS/PSS, there may be an untaxed component. Any untaxed components will continue to be taxable regardless of age. If you are over 60, you may be eligible for a 10% tax offset on tax you pay personally.

Accessing Superannuation – 65 and over

The basic conditions of release are:

- Reaching age 65

- Retirement

- Permanent incapacity, or

- Terminal medical condition

There are other more specific conditions of release however these are the most common.

If you are yet to retire and have a TRIS upon reaching age 65, the TRIS will convert automatically to an ABP (subject to the Transfer Balance Cap). At this point the pension will be in retirement phase, and withdrawals, earnings and capital gains will all be tax-free.

If you have already commenced an ABP, the tax treatment will continue to be tax-free.

Interaction with Transfer Balance Cap

The transfer balance cap is a limit on the total amount of superannuation that can be transferred into the retirement phase. The current cap is $1.6million. This will be indexed periodically. If, however, you meet or exceed the cap, you will not be entitled to indexation.

When commencing a retirement phase income stream (i.e. ABP), it is important to consider the balance at commencement date. If your funds are above $1.6million, you will be required to leave some amounts in accumulation.

As a result of this cap on retirement phase, members with large superannuation balances may continue to pay tax on earnings and capital gain on money within the accumulation phase.

However, any withdrawals made from accumulation after age 60 will continue to be tax free.

Accessing Superannuation – How can Waterhouse Lawyers help you?

If you have any questions about accessing your super or illegal early access of superannuation, Waterhouse Lawyers can help you. Our lawyers and advisors have provided many clients with advice on their superannuation issues. Please contact us on 02 9252 8746, tax@waterhouselawyers.com.au or via our inquiry form.

Related Articles

SMSF Trustee Disqualification: Legal & Tax Guide

Picture this: In the complex world of superannuation you decide to take charge of your retirement savings by establishing a Self-Managed Superannuation Fund (SMSF) but then […][…]

Bringing your super to Australia from overseas

Transferring Foreign Superannuation. When people relocate to Australia, superannuation is sometimes forgotten. Depending on when you bring back your super to Australia, and how much, it […][…]

Credentials

Recognition