- TAX LAWYERS, TAX ADVISORY, TAX COMPLIANCE, EXPATS - SYDNEY, BRISBANE, MELBOURNE, CANBERRA

- 1300 334 518

- admin@waterhouselawyers.com.au

NSW Land Tax Refund for Eligible Countries: Latest Updates

Tax Advice

NSW Land Tax Refund for Eligible Countries: Latest Updates

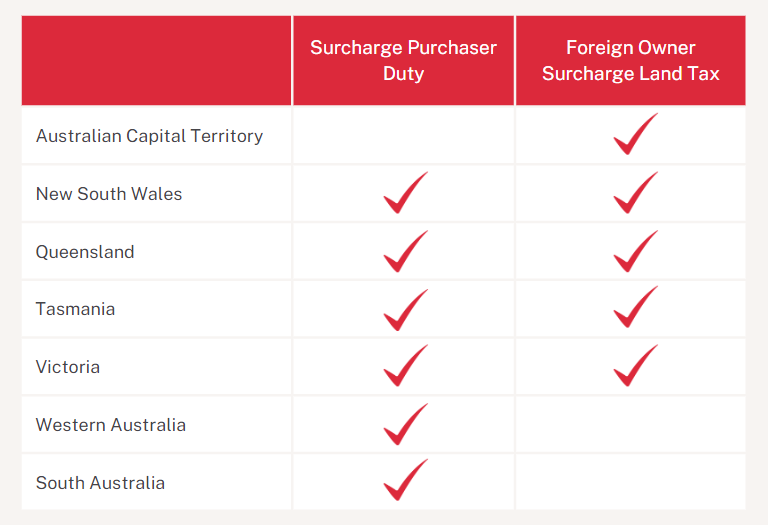

Accessing NSW Land Tax Refunds

Accessing NSW Land Tax Refunds

The revised regulations not only benefit individual purchasers but also extend to non-individual entities such as corporations, partnerships, and trusts affiliated with the listed nations. This shift in policy reflects a broader commitment to aligning with international tax treaties and promoting fair taxation practices.

Updates and Potential Ramifications

While NSW has made strides in rectifying inconsistencies, other states like Victoria maintain their stance on foreign purchaser duties and absentee owner surcharges. The divergence in approaches between states raises questions about the underlying reasons and potential implications for taxpayers.

Waterhouse Lawyers Can Help

Related Articles

Simplified Transfer Pricing Record Keeping

Simplified transfer pricing record keeping can save an Australian entity with a related offshore entity a lot of time and money. If an Australian entity qualifies […][…]

BAS Refund Fraud

Are you a victim of BAS Refund Fraud. Or perhaps have lodged BASs that falsely claimi expenses? If you are a victim we can help by […][…]

Credentials

Recognition