- TAX LAWYERS, TAX ADVISORY, TAX COMPLIANCE, EXPATS - SYDNEY, BRISBANE, MELBOURNE, CANBERRA

- 1300 334 518

- admin@waterhouselawyers.com.au

Setting up your sole trader business for success

Tax Debt

Setting up your sole trader business for success

I help a lot of sole traders to deal with their tax debt. Often, they don’t have a system in place to save for tax, and they come unstuck early in their business.

Here are 3 steps a sole trader can take to prepare their business for tax success.

The sooner you take these steps, the better. But it’s never too late to start.

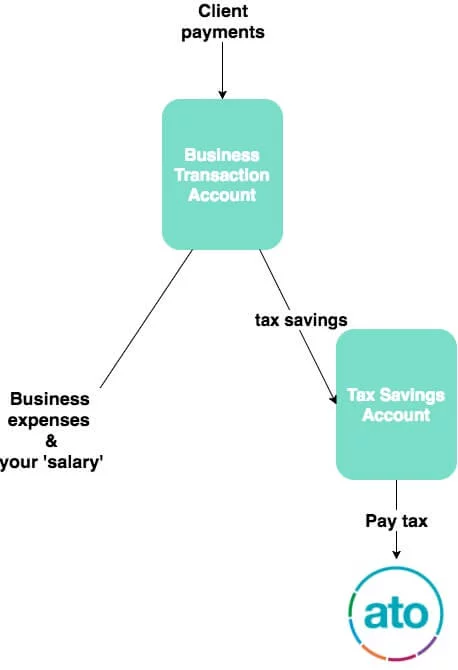

Step One – set up two separate business accounts

The first thing you should do is have two separate accounts for your business – one for expenses, one for tax. Set these up as soon as possible.

This diagram shows how you will use these two accounts in your business:

Business Transaction Account

The first account is for your business transactions.

Your clients pay into your Business Transaction Account. You pay your business expenses out of this account.

Your Business Transactions Account should only be used for business income and expenses. Don’t start putting your groceries through this account. This makes it harder to get your taxes right later.

The reason that you want a separate account just for business expenses is to make it easy to do your tax returns and BAS. You will know that all the transactions are business related income or expenses. You don’t need to spend time working out whether the $55 spent at Bunnings was for work materials, or a private project on your house.

The goal is to keep things as simple as possible. The easier you make it for yourself, the more likely you are to get your tax returns and BAS lodged on time.

Tax Savings Account

The second account is for your tax. You’ll be putting money into this account regularly to save for the tax you have to pay in the future.

I recommend that you don’t get an ATM card with this account. You don’t want to be tempted to spend your tax money.

Think you might be tempted to access this money by simply transferring into an account that has an ATM card? Then set your Tax Savings Account up with a completely different bank. It will usually take 1 or 2 business days for any transferred funds to become accessible. The harder this money is for you to spend, the more likely you are to keep it for it’s real purpose – tax.

Step Two – work out how much you should be saving for tax

Working out how much you need to save for tax can be a bit tricky. There are no neat formulas.

Remember, even though it’s hard to know exactly how much tax you will have to pay, you should still save something towards tax.

Here’s how I suggest you work it out.

Income tax

In the first year of your business, try to estimate how much you will earn.

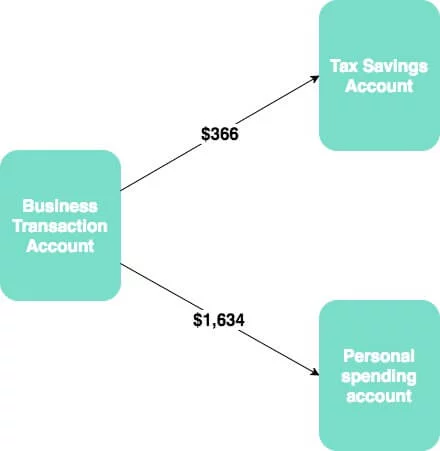

Let’s say you think you will earn $52,000 a year (after expenses). That’s an average of $2,000 a fortnight.

Go to paycalculator.com.au and put this figure into the ‘Your Salary’ box. This gives you a breakdown of what your tax will be on a weekly, fortnightly, monthly and annual basis.

I recommend you pay yourself and save your tax on a fortnightly basis.

So, for an income of $52,000 a year, the calculator says you would have tax of $366 per fortnight and your after tax income would be $1,634.

You should set up a scheduled transfer for these amounts. That is, every fortnight, you transfer $366 from you Business Transaction Account into your Tax Savings Account.

You would also transfer $1,634 from your Business Transaction Account into your personal account every fortnight. This is what you will use for groceries

and other private expenses.

Keep an eye on your income and re-do your calculations every few months.

If you earn a lot more than expected, then you may want to pay yourself a ‘bonus’ into your personal spending account. If you do this, remember to allocate an amount for income tax as well and put it in your Tax Savings Account.

If you earn less than expected, then reduce the regular payments for the future.

GST

GST can be a little bit harder to work out. But, just because it’s difficult, doesn’t mean you should ignore it.

Remember, you’re trying to set yourself up for success – and success takes effort.

There are two ways to do this. The easiest option is to just save 10% of every invoice. This means you are ignoring the fact that you will get GST credits on your business expenses. For example, when you spend $55 at Bunnings on some materials for a job, $5 of this will be GST. You will get a $5 credit for this GST which you can offset against the GST you collect from your customers.

Example

Jason receives a total of $22,000 in payments from customers during the quarter. He has saved 10% of each invoice into his Tax Savings Account – so he has $2,000 tucked away for GST.

In the same quarter, Jason paid $600 in GST on supplies, petrol, etc. He gets GST credits for this GST. That is, the GST he paid on these expenses gets offset against the GST he collected.

When Jason prepares his BAS, he finds that the GST he has to pay for the quarter is only $1,400 – because of the credits he received.

| Sep 2017 Quarter | |

|---|---|

| GST collected from clients | $2,000 |

| less GST paid on business purchases | -$600 |

| GST payable to ATO | $1,400 |

This means Jason saved $600 more than he needed. He can transfer this out to his personal account and enjoy the bonus.

The second option is more difficult. Under this option, you would try to account for the GST credits before you save the GST money.

For example, if you estimate that you spent $660 on materials for a $2,200 job, then you would have GST credits of $60 to offset against the GST collected of $200. So you might only transfer $140 into your Tax Savings Account.

Your calculations for each invoice would look something like this:

| GST on invoice #12345 | |

|---|---|

| GST collected on invoice | $200 |

| less estimated GST paid on materials for job | -$60 |

| Amount to deposit to Tax Savings Account | $140 |

This can be more difficult to calculate. You would need to do it for each invoice and some expenses may relate to more than one specific invoice (for example, petrol).

You may just prefer to save a fixed percentage of every invoice – e.g. 7-8%. You will need to do some calculations to work out what the ‘right’ percentage it.

Remember that you will never get it perfect. Just make a reasonable estimate and start saving that amount. You’ll be in a much better position than if you do nothing.

PAYG withholding and superannuation

If you have employees, then you also need to set aside money for their PAYG withholding and superannuation.

This should be pretty straightforward.

You can use the ATO tax tables to work out how much to withhold from each pay packet.

The superannuation is currently 9.5% of their salary or wage.

Transfer the PAYG withholding and superannuation to your Tax Savings Account when you’re processing payroll. Do this straight away so that you don’t get tempted to spend this money.

If you pay your employees a salary, then set this up as an automatic scheduled payment to make life easier. The easier you make it on yourself, the better your chances of success.

Remember – it will never be perfect

You need to accept that you will never get this perfect. And that’s totally okay.

The important thing is that you have a good chunk of your tax saved for tax time. If there’s a shortfall, it should only be small and you should be able to make it up. If you can’t make it up, then you need to do two things:

- Call the ATO as soon as possible and negotiate a payment plan for the rest of the tax debt.

- Re-look at your calculations so that you have enough next time.

Don’t give up. Don’t decide that it’s too hard so you’re not going to save anything. This doesn’t end well and the ATO will come looking for their money.

Step Three – lodge on time

If you’ve done steps one and two, then step three should be easy.

Do your lodgements. Do them on time.

You can download the ATO app which has a list of ‘Key dates’ for lodgement. You can even ask the app to set a reminder for all key dates – it will add these into your phone’s calendar. You will then be reminded about each due date, 7 days in advance.

If you hate paperwork, then get someone to help. You can get a bookkeeper to look after your BAS and an accountant to look after your tax returns. Or an accountant can look after both your BAS and tax returns.

The other thing to remember is that you should still lodge even if you haven’t saved enough to pay your tax. If you don’t, the ATO can prosecute you for not lodging … and you’ll still have to pay the tax. Also, the ATO is going to be more open to negotiating a payment plan if you have a history of lodging on time.

Final thoughts

Running your own business can be tough, but it can also be very rewarding. Following these three simple steps will help you to get your tax obligations right.

It’s never too late to put these steps in place, even if you’ve already been in business for a while.

This article is not legal advice; it is a brief summary of a complicated topic.

RELATED ARTICLES:

Credentials

Recognition