- TAX LAWYERS, TAX ADVISORY, TAX COMPLIANCE, EXPATS - SYDNEY, BRISBANE, MELBOURNE, CANBERRA

- 1300 334 518

- admin@waterhouselawyers.com.au

Remission of the general interest charge – the tax consequences

Tax Debt

Remission of the general interest charge – the tax consequences

When you don’t pay a tax debt on time, the ATO imposes a ‘general interest charge’ (the GIC).

The ATO has the discretion to remit the general interest charge (i.e. remove it from your account). The law is very specific about when the ATO can allow a remission. You should be careful when you make a request, so you put yourself in the best position for success. If you owe a lot of GIC, I recommend speaking to a tax dispute expert for help with making an application.

If an application is made and the ATO grants the remission – great! The ATO will take this amount off your tax debt.

But that is not the end of it. You could end up having to pay tax on the remitted amount.

To explain this, let’s start with the rules about how the tax law applies when the general interest charge is first imposed.

Deduction for the general interest charge

The general interest charge on income tax debts is tax deductible as a tax-related expense. It is deductible when it is charged – which is when it shows up on your Statement of Account.

This means that if you are charged $10,000 of GIC in an income tax year, you can claim a tax deduction for that $10,000.

This is the case even if you haven’t actually paid the GIC to the ATO – the fact that you have incurred it as a debt means that it is deductible.

You pay tax on a remitted GIC if you can claim a deduction

If you apply for a remission of the GIC and it is granted, then the ATO reduces your tax debt by the remitted amount.

The tax law says that if you recoup an amount that was deductible, then the recoupment is assessable. Put another way, the remitted GIC is assessable to tax in two situations:

- If you have claimed a deduction for the GIC

- If you can claim a deduction for the GIC

These amounts are assessable income for the tax year that the ATO granted the remission.

The only remitted GIC that is not assessable income is GIC for which you cannot claim a deduction.

Example of when you can, and cannot, claim a deduction for the GIC

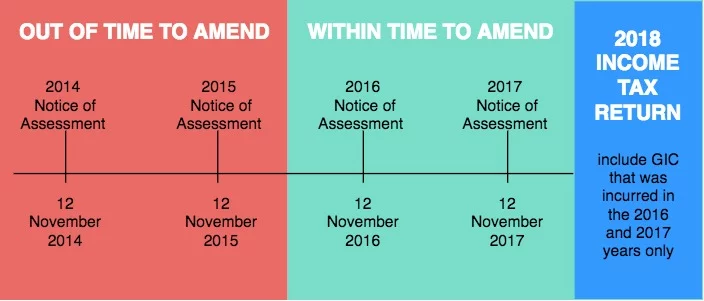

Bonnie had a tax debt from her 2013 tax return that she didn’t pay for a long time. Each year, more and more GIC is charged to her account.

She lodged her returns for the following years on time and the ATO issues her a Notice of Assessment on 12 November of each year.

She didn’t claim a deduction for the GIC in any of her tax returns.

In October 2017, Bonnie received an inheritance and paid off her old tax debt.

She sought tax advice about what could be done about the general interest charge. Her tax lawyer asked the ATO to remit all the GIC that Bonnie had incurred over the years on it.

The ATO agreed and granted the full remission on 23 November 2017.

Even though Bonnie hasn’t claimed a deduction for the GIC, the remitted amount is assessable if she can claim a deduction.

So Bonnie needs to know if she can claim a deduction for any of the GIC. Here’s what she finds out:

- She can claim a deduction for the GIC incurred in the 2016 and 2017 income years. This is because less than 2 years have passed since the notice of assessment for those years was issued*. This means she can deduct the GIC for those years by amending the tax returns.

- She cannot claim a deduction for the 2014 and 2015 income years because she is out of time to amend her 2014 and 2015 income tax returns.

*Note, the time limit for amending a return is either 2 years or 4 years from the date of the Notice of Assessment, depending on what sort of taxpayer you are.

She should go back and amend the 2016 and 2017 tax returns to actually claim the deduction for the GIC incurred in those years. She should then include the same amount of GIC as assessable income in her 2018 tax return.

She should not include the GIC incurred during the 2014 or 2015 income years as assessable income in the 2018 return.

Bonnie could decide not to go back and amend the 2016 and 2017 tax returns. But, she would still have to report the remitted GIC that she incurred in those two years as assessable income. This means she would pay tax on the remitted amounts and would be out of pocket.

The overall effect

The overall effect of this is to cancel out the deduction in the first place. You end up neither better nor worse off after having the general interest charge remitted.

If you have claimed the deduction in the past, then your next tax return after the deduction is going to be higher than usual. This is because it includes the ‘extra’ income of the remitted GIC. It’s important to be aware of this so that you can plan for the extra tax.

But don’t let this scare you off seeking a remission of interest. It is much better to be paying a percentage of tax on the remitted GIC than it is to have to pay 100% of the GIC!

RELATED ARTICLES:

Credentials

Recognition