- TAX LAWYERS, TAX ADVISORY, TAX COMPLIANCE, EXPATS - SYDNEY, BRISBANE, MELBOURNE, CANBERRA

- 1300 334 518

- admin@waterhouselawyers.com.au

Proposed Budget changes for taxing discretionary trusts

Tax Advice

Proposed Budget changes for taxing discretionary trusts

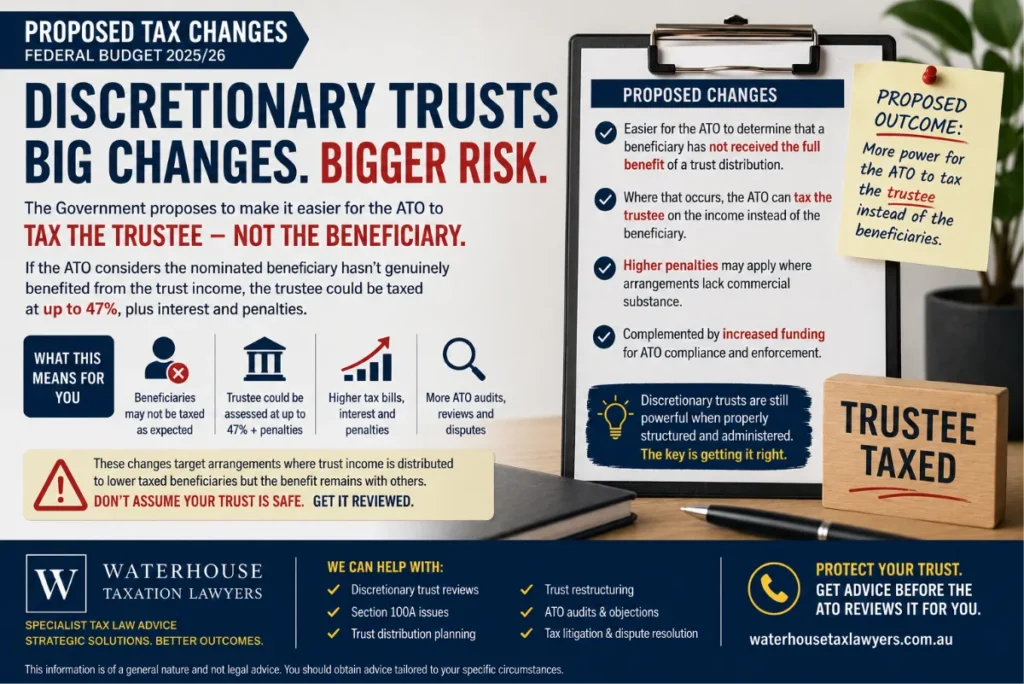

The Federal Budget has proposed major tax changes for discretionary trusts, and from 1 July 2027 the way trusts are taxed in Australia could change significantly.

Under the proposed reforms, discretionary trust income may no longer be taxed in the hands of the beneficiaries at their individual marginal tax rates. Instead, it is proposed that certain trust distributions will be taxed directly to the trustee at a flat rate of 30%.

This is a major shift from the traditional way discretionary trusts have operated for decades.

Historically, trustees could distribute trust income between family members, adult children or related entities depending on each person’s tax position. For many business owners and investors, this flexibility has been one of the main benefits of using a discretionary trust.

The proposed changes are aimed at reducing what the Government considers to be “income splitting” through family trust structures.

In simple terms, the Government’s concern is that some higher income earners have been distributing trust income to lower taxed beneficiaries to reduce the overall family tax bill.

If implemented, the proposed rules could significantly reduce the tax effectiveness of discretionary trusts for many families and private business groups.

The changes are expected to particularly impact:

- family business structures;

- investment trusts;

- professional service firms;

- property investors; and

- high-income family groups using discretionary trusts.

Importantly, the proposed 30% trustee tax model may apply regardless of whether the beneficiary personally receives the funds.

Combined with the ATO’s existing focus on section 100A, unpaid present entitlements (“UPEs”), Division 7A and reimbursement agreements, trustees are facing increasing scrutiny from multiple directions.

The Federal Budget also included additional ATO funding for audit and compliance activity targeting private groups and trust structures. This means more audits, more reviews and greater scrutiny of historical trust distributions over the coming years.

While the proposed changes are not yet law, many accountants, advisers and business owners are already reviewing existing structures ahead of the proposed commencement date of 1 July 2027.

For some taxpayers, restructuring early may become important to avoid future tax issues and unexpected liabilities.

Importantly, discretionary trusts are still valuable structures for asset protection, succession planning and business flexibility. However, the tax advantages may look very different if the proposed reforms proceed.

At Waterhouse Taxation Lawyers, we assist clients with:

- discretionary trust restructuring;

- tax planning advice;

- section 100A disputes;

- ATO audits and objections;

- family group restructuring; and

- trust taxation disputes and litigation.

If you operate through a discretionary trust, now is the time to review your structure and understand how the proposed 2027 tax changes may affect your family or business.

Related Articles

Tax Residency: the 183-day test is just the beginning

Residency: 183-day test Many people think that if they satisfy the 183-day residency test then they satisfy the tax residency test. Wrrrrrong. The 183 day test […][…]

Small Business CGT (Capital Gains Tax) Concessions

The Small Business CGT (Capital Gains Tax) Concessions in Australia provide tax relief for eligible small businesses when selling active assets. These concessions can significantly reduce […][…]

Credentials

Recognition